Rural real estate future not clear: REINZ

28 July 2020, 1:02 AM

Dairy farm sales have been quiet in Southland: PHOTO: Dairy NZ file photo

Dairy farm sales have been quiet in Southland: PHOTO: Dairy NZ file photoIt is not clear what the future might hold for farming but it is clear rural investors are seeking better returns, Real Estate Institute of New Zealand spokesman Brian Peacocke says.

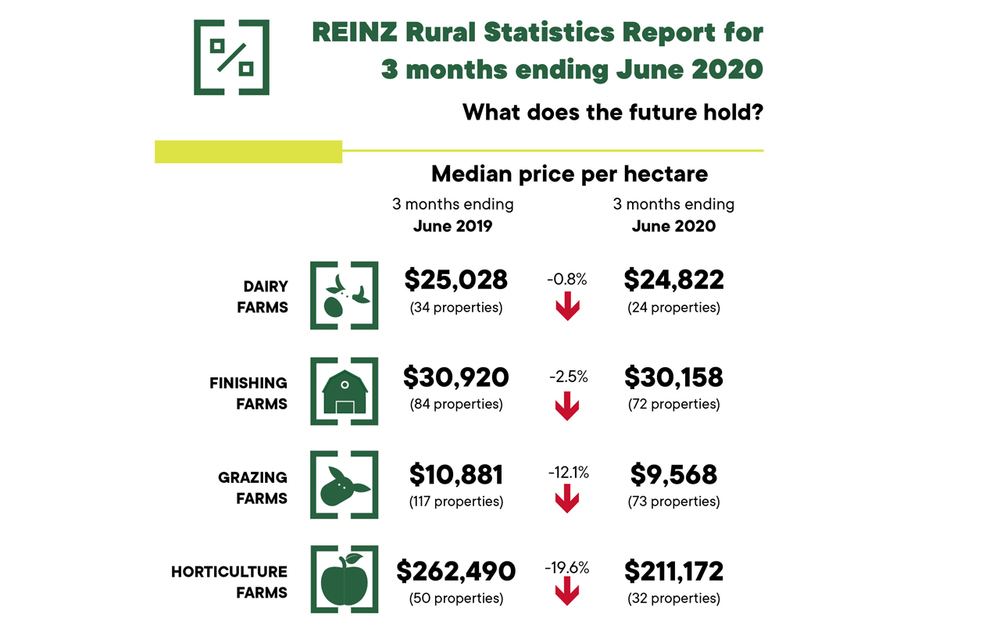

The number of farms sales was down during the three months to June, according to REINZ data released this month.

Mr Peacocke said there was steady activity in Otago and Southland, with solid prices paid for finishing, grazing and arable properties in the Dunedin and Clutha districts.

“[And] not to be outdone by their northern neighbours, [there was] a solid flourish of strongly priced sales of finishing, grazing and arable properties in the Southland and Gore districts; [but] very quiet throughout within the dairy scene,’’ Mr Peacocke said.

The drop in national farm sales numbers for the June quarter continued an established trend.

So far this year, there have been 1154 farm sales, 13.9% fewer than were sold in the year to June 2019.

There were 261 farm sales in the three months ended June 2020, 61 fewer (-18.9%) than for the same period in 2019.

Between 2015 and 208, national farm sale numbers in the June quarter gradually reduced from 479 to 427 before dropping more sharply to 322 in 2019 and falling again to 261 this year.

The median price per hectare for all farms sold in the June quarter was $23,136, compared to $22,044 for three months ended June 2019 (+5.0%).

Mr Peacocke said it was not clear if the sales slide would stabilise or the downward trend would continue.

“Should it be the latter, given the range of issues currently impacting on the rural sector, not the least being the need for youthful rejuvenation of the farm ownership structure, it could be that an avalanche of potential sales is building up . . . Irrespective of the outcome, what is clear is that the current average return on investment for those with investment in the rural sector will need to improve or there will be a decreasing incentive for attracting much needed, affordable capital into the agricultural sector.”

However, the horticultural industry is buoyant, and beef and lamb prices remain solid in spite of seasonal volatility.

The dairy industry, although quiet, has received a welcome shot in the arm from the most recent Global Dairy Trade auction, with overall prices up 8.3% in early July.

“Regrettably, the deer industry, and venison in particular, sits in uncertain territory with COVID-19 issues causing restaurants in Europe and other countries to cease ordering the product. As to how long this situation lasts, only time will tell. In the meantime, however, velvet appears to be weathering the storm,” Mr Peacocke said.

Points of interest in the South Island included reasonable activity on Marlborough sauvignon blanc vineyards and grazing blocks, supported by solid prices for a Tasman finishing block and a Kaikoura dairy support unit.

Strong prices were paid for mid-Canterbury arable and finishing properties.

The West Coast had good results for dairy support and grazing units and recorded the only sale of a dairy unit in New Zealand in June.

Nationally, grazing farms and finishing farms both accounted for the largest number of sales in the June quarter (28%), dairy accounted for 9% and horticulture accounted for 12%.